Several factors impact option prices, so traders should understand what drives these changes—including the “Greeks,” which measure risks like price movements, time decay, and volatility sensitivity. The four key Greeks to know before trading options are Delta, Gamma, Vega, and Theta.

Delta Δ (Price Sensitivity) : Rate of Change of Underlying

An option’s delta measures how much an option’s price is expected to change based on a $1 increase in the price of the underlying asset.

The value of delta is between −1 and 1.

Call options: a positive delta between 0 and 1.

Put options: a negative delta between −1 and 0.

Example: In the event that the price of the underlying asset increases by $1:

Delta = 0.3

The price of the option is expected to increase by $0.30.

Delta= − 0.2

The price of the option is expected to decrease by $0.20

Gamma Γ (Delta Sensitivity)

Gamma is a measure of how much the Delta is expected to change when the price of the underlying asset rises by $1. The higher the Gamma, the more the option Delta will change, which means the greater the change in the option price.

Example: In the event that the price of the underlying asset increases by $1:

Delta = 0.3, Gamma = 0.1

Delta will increase from 0.3 to 0.4, which means that the price of the option is expected to increase by $0.30 to $0.40.

Theta Θ : Time Decay

Theta measures the expected change in the value of an option over time. Simply put, it indicates how much value the option is expected to lose each day as it approaches expiration.

Theta is always negative for call and put option buyers, as the closer the option is to expiring, the less value the contract has. In addition, the higher the negative Theta, the greater the loss in value of the option is expected to be the next day.

Example

Theta = −1.5

All other factors being equal, the option is expected to lose $1.50 in value the next day.

Vega: Volatility Sensitivity

Vega measures how much an option’s price will change for a 1% change in the implied volatility of the underlying asset.

Example:

Vega = 12

It’s expected that a 1% increase in implied volatility will cause the option price to increase by $12. If the implied volatility decreases by 1%, it will cause the option price to drop by $12.

Implied Volatility (IV): Future Volatility of Underlying Price

While implied volatility (IV) isn’t technically Greek, it’s a key metric linked to option pricing. IV reflects the market’s expectations of future volatility for the underlying asset. The higher the IV, the greater the anticipated price swings—leading to higher option prices, so buyers pay more premiums and sellers earn more. If IV is lower, option prices and premiums decrease.

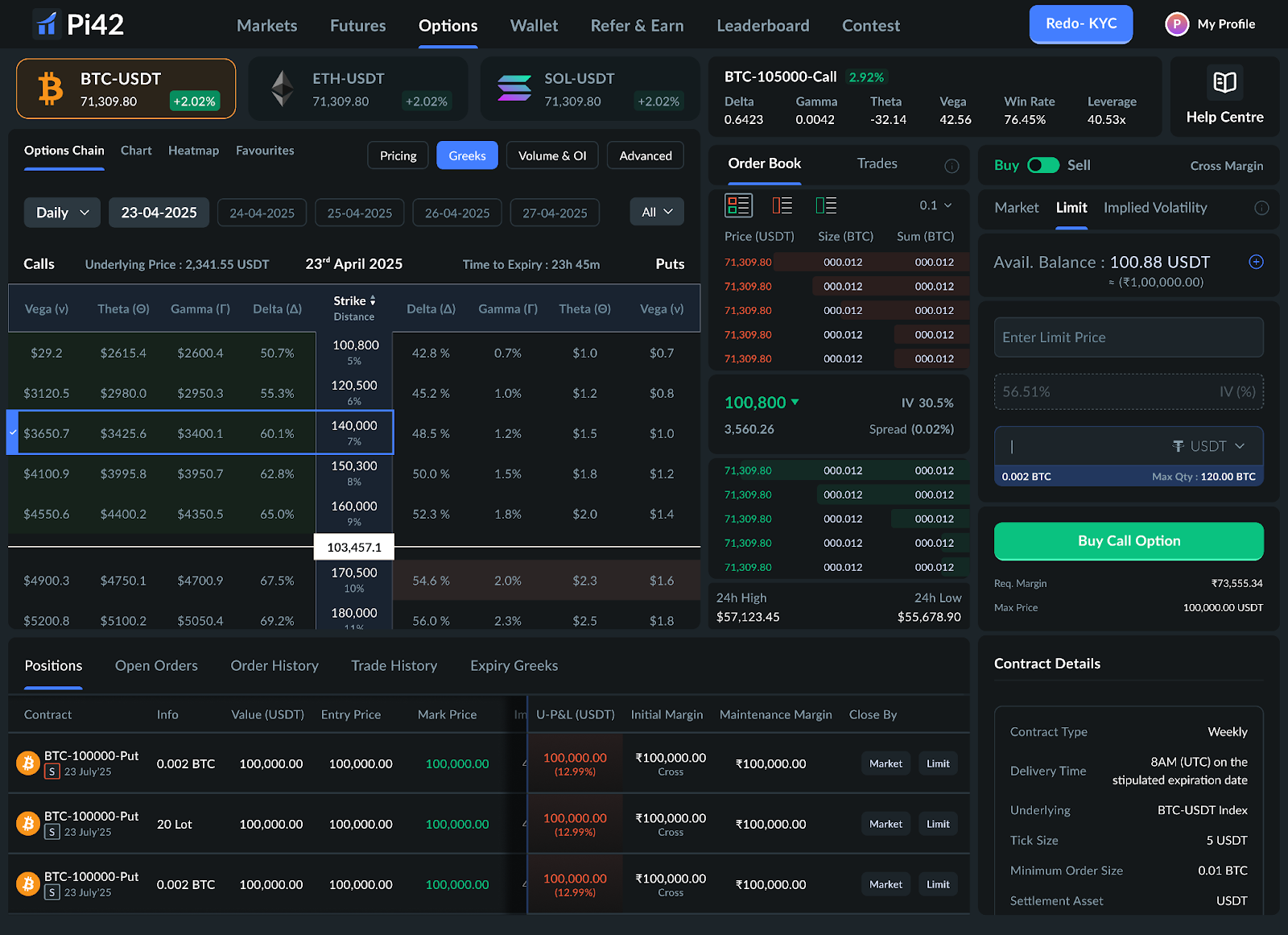

Where can I see the Greeks on Pi42?

Options Chain

You can see the Greeks Tab on the Option Chain page. This tab shows the Greeks values for each option strike. The left column is for call options, and the right column is for put options.

Was this article helpful?

That’s Great!

Thank you for your feedback

Sorry! We couldn't be helpful

Thank you for your feedback

Feedback sent

We appreciate your effort and will try to fix the article